Adobe PDF

Adobe PDF

Laws

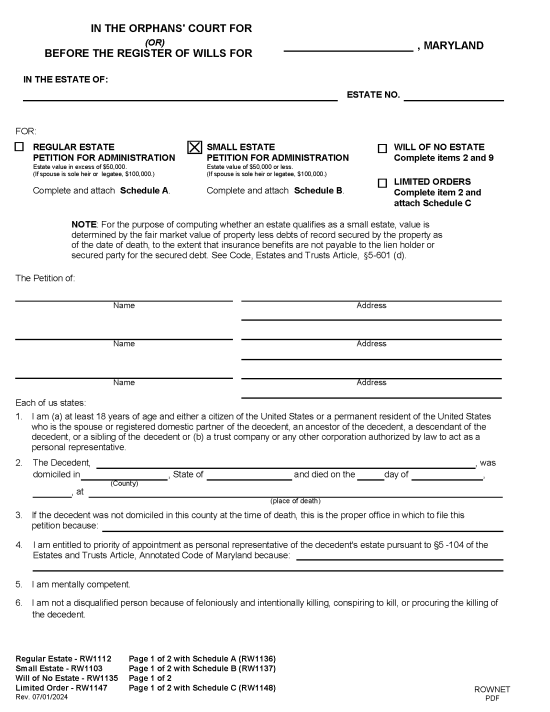

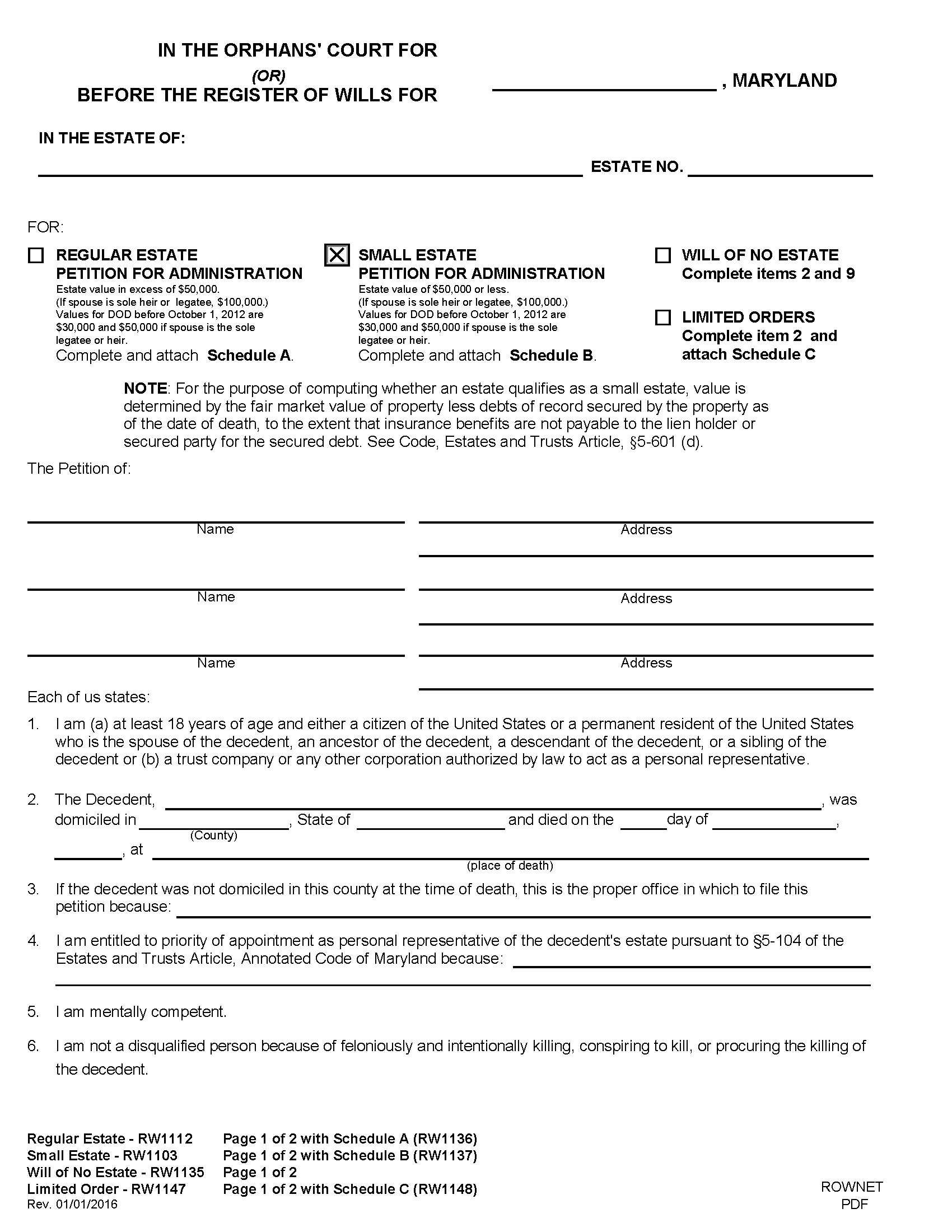

- Maximum Estate Value: $50,000 ($100,000 if the surviving spouse is the sole heir or legatee)[1]

- Mandatory Waiting Period: None

- Where to File: Orphans’ Court or Register of Wills

How to File (4 Steps)

Step 1 – Prepare Documents

The petitioner for appointment of personal representative will need the following documents to open a small estate[2]:

- Last Will and Testament and Codicil(s) (if any)

- Copy of the Death Certificate – Obtained from the Division of Vital Records

- Documentation of any funeral expenses

- Petition for Administration of a Small Estate

- Schedule – B

- List of Interested Persons

- Consent to Appointment of Personal Representative

- All interested persons with a higher priority to serve than the petitioner must complete this form.

- Notice of Appointment / Notice to Creditors / Notice to Unknown Heirs

- Appointment of Resident Agent

- Complete if the petitioner does not reside in Maryland.

- Information Report

- The personal representative must file within three months of their appointment.

- Bond of Personal Representative

- For estates valued $10,000 or more. Not required if stated in the will, or all interested persons sign a Waiver of Bond.

- Affidavit of Attempt to Comply With Federal, State, and Local Laws Related to Firearms, Ammunition, and Destructive Devices

Certain jurisdictions may have additional requirements for opening a small estate. The petitioner should check with the Register of Wills in the jurisdiction where the decedent lived to confirm their requirements.[3]

Step 2 – File Documents

The Petition and supporting documents will be filed with the Register of Wills in the county where the decedent resided. If there are questions regarding the validity of the will, the estate may need to be administered by the Orphans’ Court.[4]

Step 3 – Personal Representative

If the petitioner is appointed as personal representative, they will be issued Letters of Administration and information about their estate management obligations.

The personal representative will be required to file an Information Report within three months of their appointment and an Application to Fix Tax on Non-Probate Assets no later than 90 days after the decedent’s passing.

Step 4 – Distribute Assets

Once all requirements are met, the personal representative may distribute assets according to the terms set in the decedent’s will or intestacy laws.