Adobe PDF

Adobe PDF

Microsoft Word

Microsoft Word

OpenDocument

OpenDocument

An adverse action notice informs the applicant of their rights, which includes their access to a free credit report as long as it is requested within sixty (60) days of the rejection. Prior to the adverse action report, the sending entity will often deliver a pre-adverse action notice. This provides the recipient with ample time to correct any issues in the credit report to obtain reports.

Contents |

Sample

Download: PDF, Word (.docx), OpenDocument

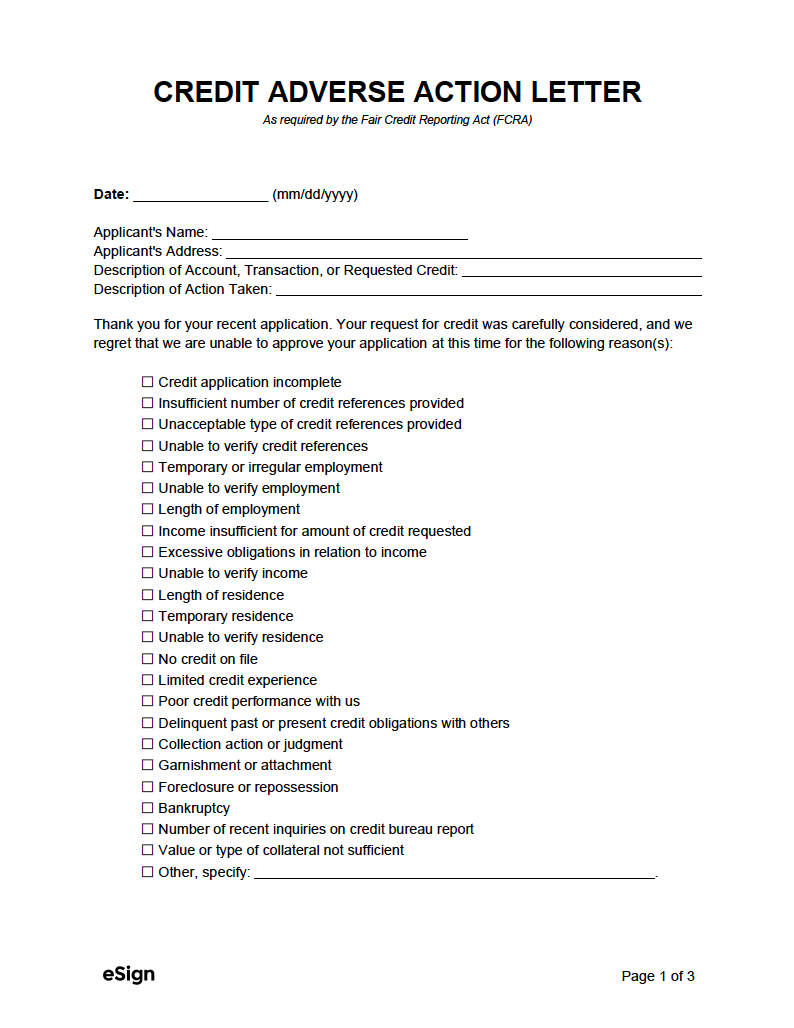

CREDIT ADVERSE ACTION LETTER

As required by the Fair Credit Reporting Act (FCRA)

Date: [MM/DD/YYYY]

Applicant’s Name: [APPLICANT NAME]

Applicant’s Address: [APPLICANT ADDRESS]

Description of Account, Transaction, or Requested Credit: [ACTION TAKEN]

Description of Action Taken: [DESCRIBE WHY THE ACTION WAS TAKEN]

Thank you for your recent application. Your request for credit was carefully considered, and we regret that we are unable to approve your application at this time for the following reason(s):

☐ Credit application incomplete

☐ Insufficient number of credit references provided

☐ Unacceptable type of credit references provided

☐ Unable to verify credit references

☐ Temporary or irregular employment

☐ Unable to verify employment

☐ Length of employment

☐ Income insufficient for amount of credit requested

☐ Excessive obligations in relation to income

☐ Unable to verify income

☐ Length of residence

☐ Temporary residence

☐ Unable to verify residence

☐ No credit on file

☐ Limited credit experience

☐ Poor credit performance with us

☐ Delinquent past or present credit obligations with others

☐ Collection action or judgment

☐ Garnishment or attachment

☐ Foreclosure or repossession

☐ Bankruptcy

☐ Number of recent inquiries on credit bureau report

☐ Value or type of collateral not sufficient

☐ Other, specify: [OTHER REASON].

☐ (Check if applicable). Our credit decision was based in whole or in part on information obtained in a report from the consumer reporting agency listed below. You have a right under the Fair Credit Reporting Act to know the information contained in your credit file at the consumer reporting agency.

The reporting agency played no part in our decision and is unable to supply specific reasons why we have denied credit to you. You also have a right to a free copy of your report from the reporting agency, if you request it no later than 60 days after you receive this notice. In addition, if you find that any information contained in the report you receive is inaccurate or incomplete, you have the right to dispute the matter with the reporting agency.

Reporting Agency Name: [REPORTING AGENCY NAME]

Reporting Agency Address: [REPORTING AGENCY ADDRESS]

Reporting Agency Telephone number (Toll-Free): [REPORTING AGENCY PHONE]

We also obtained your credit score from this consumer reporting agency and used it in making our credit decision. Your credit score is a number that reflects the information in your consumer report. Your credit score can change, depending on how the information in your consumer report changes.

Your credit score: [#]

Date: [MM/DD/YYYY]

Scores range from a low of [#] to a high of [#].

Key factors that adversely affected your credit score:

- [FACTOR 1]

- [FACTOR 2]

- [FACTOR 3]

- [FACTOR 4]

- Number of recent inquiries on a consumer report, as a key factor.

If you have any questions regarding your credit score, you should contact the entity that provided the credit score at:

Address: [ENTITY ADDRESS]

Telephone number (Toll-Free): [PHONE NUMBER]

| (Check if applicable)

☐ Our credit decision was based in whole or in part on information obtained from an affiliate or from an outside source other than a consumer reporting agency. Under the Fair Credit Reporting Act, you have the right to make a written request, no later than 60 days after you receive this notice, for disclosure of the nature of this information. Creditor’s name: [CREDITOR NAME] |

ECRA Notice: The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age (provided the applicant has the capacity to enter into a binding contract); because all or part of the applicant’s income derives from any public assistance program; or because the applicant has in good faith exercised any right under the Consumer Credit Protection Act. The Federal agency that administers compliance with this law concerning this creditor is (name and address as specified by the appropriate agency listed in appendix A).

What is a Credit Report?

A credit report is a collection of an individual’s financial history, focusing on how they handled previous debt obligations. It is used by entities to determine if they can take on the risk of trusting a person with paying for rent, utility bills, and loan payments (to name a few examples). There are three (3) main credit reporting agencies:

- Experian

- Equifax

- Transunion

Who Can Pull a Credit Report?

Any entity can gain access to a person’s credit report if they have a justifiable reason for doing so. Entities that are known for using consumer credit reports include:

- Creditors

- Student loan providers

- Financial institutions (banks)

- Property managers (landlords)

- Utility providers.

What’s Included?

Information contained in credit reports is often categorized into the following groups:

- Accounts (most important) – Any money that is currently borrowed is included here. Credit card debt, mortgages, car loans, student loans, and so on. This also contains information on the terms of each debt and if the debtor has made timely payments.

- Public records – This includes information that is available to the public via the court system, namely bankruptcies and debts that have been sent into collections.

- Personal info – The name, address, phone number, birth date, employers, and SSN of the person being screened is available on the report.

- Recent inquiries – The number of hard credit inquiries (and when they took place) from the past two (2) years is displayed on the report.