Adobe PDF

Adobe PDF

Microsoft Word

Microsoft Word

OpenDocument

OpenDocument

State Laws

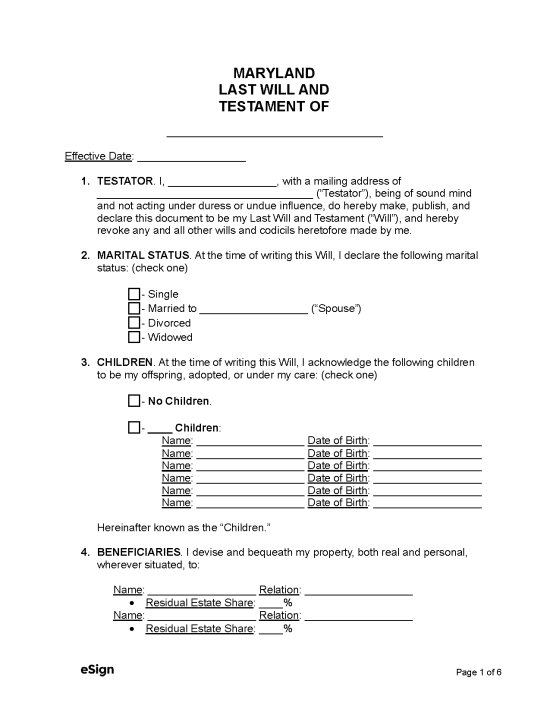

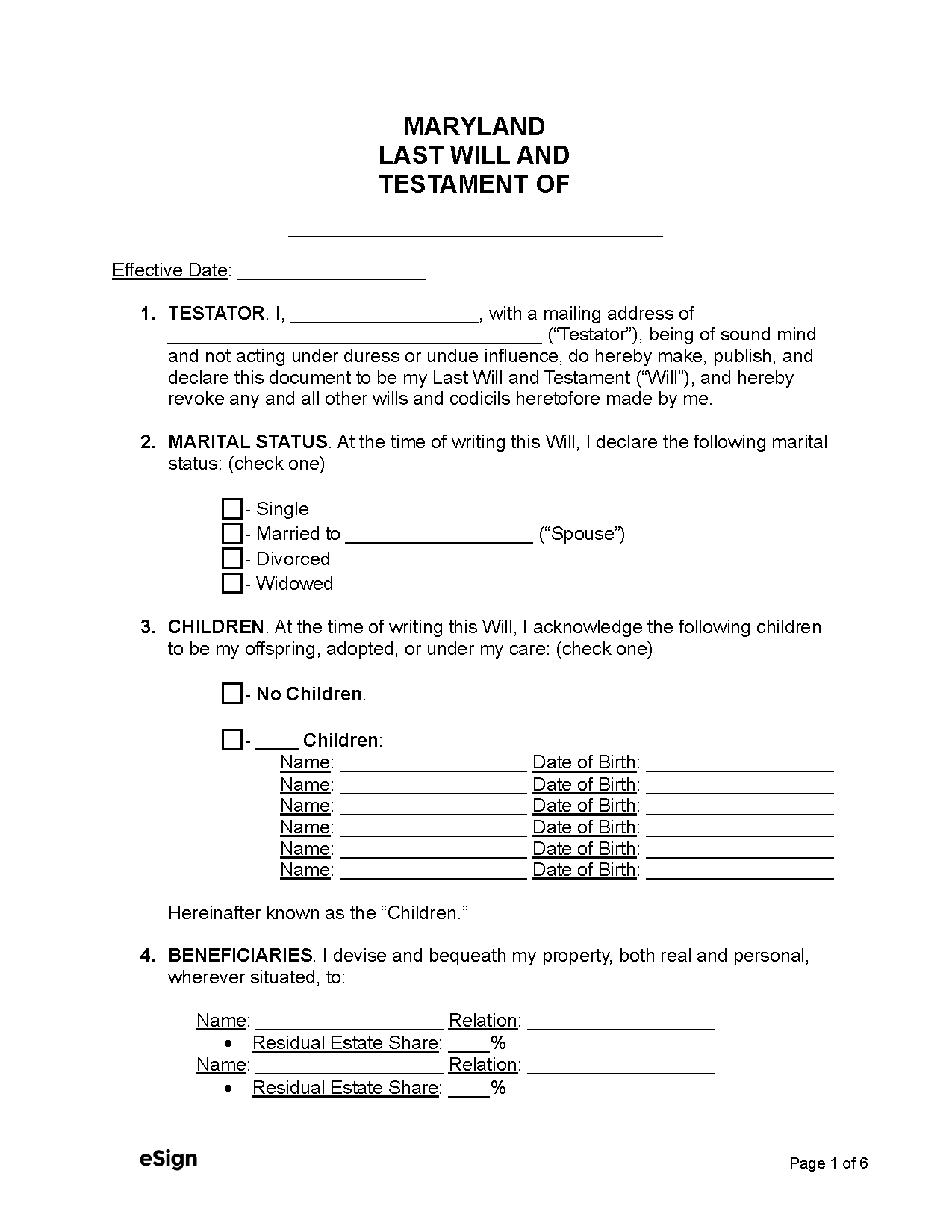

Wills may be executed by legally competent individuals at least 18 years old.[1]

Holographic Wills – Handwritten wills made outside the U.S. by members of the armed forces are valid for a year after discharge, with or without witnesses.[2] All other wills must be witnessed.

Revocation – A will may be revoked in the following circumstances:[3]

- A new will is executed.

- The testator (or someone at their direction) destroys the original will.

- The testator subsequently marries and has, adopts, or legitimizes a child (as long as the child or their descendants survive the testator).

- The testator divorces or annuls their marriage, which revokes the parts of the will applicable to the former spouse.

Signing Requirements – Wills must be signed by the testator and two credible witnesses in the testator’s presence.[4]

Probate Process in Maryland (5 steps)

In Maryland, there is no deadline after the decedent’s death for starting the probate process. It is nonetheless recommended to file for probate in a timely manner to avoid any complications.

- Open Estate

- Send Notices

- Prepare Inventory and Account

- Settle Taxes (If Applicable)

- Final Account and Distribution

The following is meant to be a general overview of the probate process. It is recommended that executors/personal representatives consult with an attorney if they’re unsure of any step.

1. Open Estate

To open an estate, the following will need to be provided to the Register of Wills of the county where the decedent last resided:[6]

- Petition for Administration (Form 1112) – This will petition the Register to open the estate for probate.

- Schedule A (Form 1136) – This provides the Register with the estimated estate value.

- Notice of Appointment (Form 1114) – This notice is provided by the Register to a local newspaper of the personal representative’s choosing.

- Nominal Bond (Form 1116) or Bond of Personal Representative (Form 1115) – Form 1116 is used if the will or all interested persons waive a bond.[7] Otherwise, Form 1115 is used, which must be executed by an insurance company.

- Waiver of Bond (Form 1117) – This form must be signed by all interested parties to waive a bond.

- List of Interested Persons (Form 1104) – This form must be filed within 20 days after the personal representative’s appointment.

- Probate Fee – A fee based on the estate value is due when filing for probate.

- Original last will and testament – The original will must be filed.

Once the documents are approved, the personal representative will be issued the Letters of Administration, granting them authority to administer the estate.

2. Send Notices

The newspaper that published Form 1114 will provide the personal representative with a notice of appointment. Copies of the notice should be provided to the Register within 20 days of their appointment, as the Register will distribute them to interested parties. The personal representative must also make efforts to identify creditors and deliver each a copy.

3. Prepare Inventory and Account

The personal representative must complete and file the Inventory (Forms 1122 and 1123) within three months of their appointment. If the estate had assets not fully owned by the decedent, the Information Report (Form 1124) must also be filed.

An account must be prepared and filed within nine months of appointment, though the Register does not provide an official form. The account must include:

- The initial estate balance (as indicated in the Inventory)

- Principal receipts

- Any change in assets after the decedent’s passing

- Income and disbursements

- Distributions and taxes

- The retained balance (if the account is not the final account)

- A verification of account (sample) provided by the Register.

If the account is not final, an updated version must be filed at whichever interval occurs first: six months from the previous account’s approval or nine months from its filing.

Furthermore, a notice of the account containing the details in the sample account’s verification must be served on interested persons.

4. Settle Taxes (If Applicable)

If the total estate value equals or exceeds $5,000,000, an estate tax is levied on assets transferred to other parties.[8],[9] If applicable, within nine months of the decedent’s death, the personal representative must complete IRS Form 706 and Form MET-1 and mail both forms with the will and certified death certificate to:

Comptroller of Maryland

Estate Tax Section

P.O. Box 828

Annapolis, MD 21404-0828

The Register collects an inheritance tax of 10% of the transferred property’s value, though it is not imposed on transfers to immediate or step-family members or transfers of $1000 or less.[10],[11] The inheritance tax is deducted from the estate tax, and the difference is the estate tax due. If the inheritance tax is equal to or exceeds the estate tax, no estate tax is owed. If applicable, the inheritance tax is due upon the estate’s distribution in the next step.

In addition to the above taxes, revenue generated by an estate is subject to federal and state income taxes; if applicable, IRS Form 1041 must be filed with the IRS, and Form 504 should be filed with the Comptroller of Maryland.