Adobe PDF

Adobe PDF

Laws

- Maximum Estate Value: $50,000 (not including real property and other exclusions)[1]

- Mandatory Waiting Period: Not mentioned in state statutes.

- Where to File: Orphans’ Court

How to File (3 Steps)

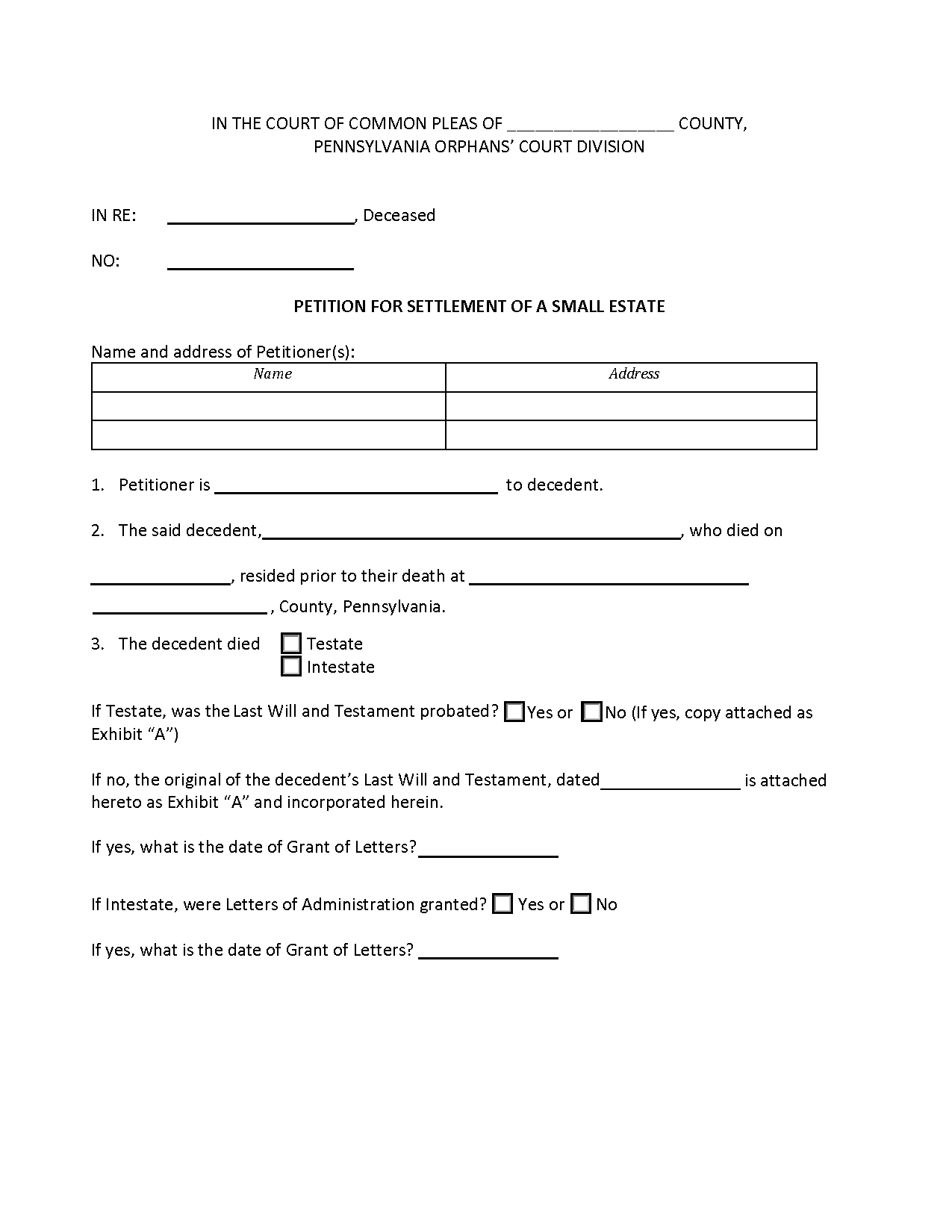

Step 1 – Estate Requirements

A Petition for Settlement of a Small Estate can only be used if an estate has a total value of $50,000 or less.[2] The following assets are not included in the estate value[3]:

- Real property

- Joint or trust accounts with survivorship

- Insurance policies or certain employee benefits with a designated beneficiary

- Wages or funds owed to the decedent that are eligible by law to be paid to family

Step 2 – File Petition

The Petition must be completed, notarized, and filed with the Orphans’ Court in the county where the decedent resided.[4] The court will then issue a Decree of Distribution, authorizing the petitioner to receive the decedent’s assets.[5]